Buying a home is the largest financial decision most families make. What many Mangaluru buyers do not fully realise is that the Indian government has built a significant set of tax benefits into that decision — benefits that, when used correctly, can reduce the real cost of ownership by lakhs of rupees over the loan tenure.

This guide breaks down every major tax benefit available to a home buyer in 2026, explains what you can actually claim, and shows you how to make those benefits work for a purchase like Udbhav Chinmaya at Kadri, Mangaluru.

One important note before we begin: most of these benefits apply only under the Old Tax Regime. If you have already switched to the New Tax Regime, speak to your CA about whether switching back makes financial sense before your next ITR filing. For most buyers with a home loan above ₹50 Lakhs, the Old Regime wins on numbers.

Table of Contents

Benefit 1 — Section 24(b): Deduction on Home Loan Interest

This is the most valuable tax benefit available to home buyers and the one most people know about but do not fully use.

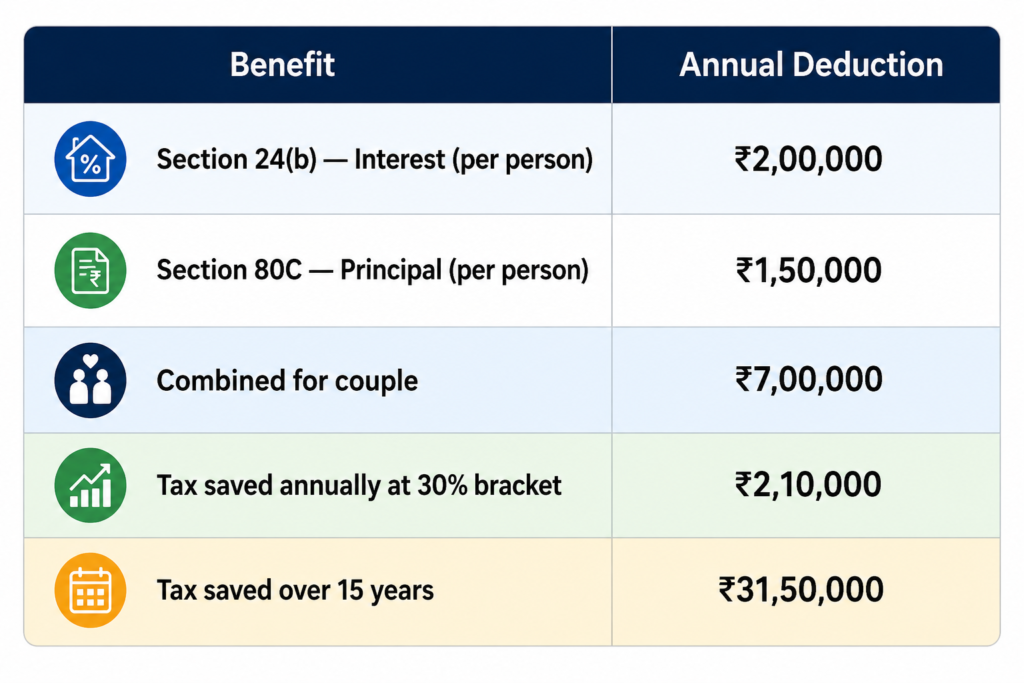

Under Section 24(b), if you live in the property for which you took the home loan, you can deduct up to ₹2 Lakh per year from your taxable income on the interest component of your EMI.

What this means in practice: if you are in the 30% tax bracket, a ₹2 Lakh interest deduction saves you ₹60,000 in tax every single year. Over a 20-year loan, that is ₹12 Lakhs in tax savings on this benefit alone — before accounting for any other deduction.

If you have rented out the property rather than living in it, there is no upper limit on the interest deduction. The full interest amount can be claimed, making rental properties even more tax-efficient for investors in higher income brackets.

Important: No deductions are available during the under-construction period. You begin claiming Section 24(b) from the financial year in which you receive possession. For Udbhav Chinmaya buyers, that means from November 2027 onwards.

Benefit 2 — Section 80C: Deduction on Principal Repayment

Every EMI has two components — interest and principal. While Section 24(b) covers the interest, Section 80C allows you to claim up to ₹1.5 Lakh annually on the principal repayment portion of your home loan.

This ₹1.5 Lakh limit is shared with other 80C investments — PPF, ELSS mutual funds, life insurance premiums, and children’s tuition fees. If your home loan principal repayment alone exceeds ₹1.5 Lakh annually, which it will at most price points above ₹50 Lakhs, your 80C is effectively maxed out from the home loan itself. You do not need separate tax-saving investments to fill that bucket.

Stamp Duty & Registration Bonus: Stamp duty and registration charges paid on purchase of a residential property are also eligible for Section 80C deduction in the year of payment, subject to the overall ₹1.5 Lakh ceiling. For a Mangaluru buyer paying stamp duty and registration on a ₹1.45 Crore apartment, this can fill a significant portion of the 80C limit in the year of purchase a one-time but meaningful saving.

Benefit 3 — The Joint Loan Advantage: Doubling Your Benefits

This is the most underutilised benefit in real estate tax planning and particularly relevant for double-income families in Mangaluru.

If your spouse is a co-owner and co-borrower, you can effectively double the Section 24(b) deduction — ₹2 Lakh plus ₹2 Lakh equals ₹4 Lakh combined — provided both partners file separate ITRs and both are repaying the EMI from their respective incomes.

Each borrower can also claim up to ₹1.5 Lakh under Section 80C, effectively doubling the combined tax benefits to ₹7 Lakh annually for a co-borrowing couple.

For a Mangaluru family buying a ₹1.45 Crore 3 BHK at Udbhav Chinmaya on a joint loan, this is not a minor saving. At the 30% tax bracket, ₹7 Lakh in combined deductions translates to ₹2.1 Lakh saved in tax every year. Over 15 years, that is over ₹31 Lakhs — nearly the cost of a modest vehicle — recovered purely through intelligent tax structuring.

Benefit 4 — Section 80EE: First-Time Buyer Deduction

In the New Tax Regime, Section 24(b) home loan interest deduction is not available for self-occupied property, and Section 80C principal deduction is also not available. This is the single biggest financial argument for choosing the Old Tax Regime if you have a home loan.

If you are paying ₹3 Lakh or more per year in home loan interest, the Old Regime almost certainly saves more total tax — even accounting for the lower slab rates of the New Regime.

For a buyer financing a ₹1.45 Crore apartment at Udbhav Chinmaya with an 80% loan of approximately ₹1.16 Crore, the annual interest in the early years of the loan will be well above ₹3 Lakh. The Old Tax Regime is almost certainly the right choice. Verify this with your CA using your exact income and slab position before filing.

Benefit 5 — Old Regime vs New Regime: The Decision That Changes Everything

Section 80EE provides an additional interest deduction of ₹50,000 per year, over and above Section 24(b), for first-time home buyers.

If you have never owned a residential property before and your loan meets the eligibility criteria — loan amount not exceeding ₹35 Lakhs and property value not exceeding ₹50 Lakhs — you can claim this on top of your regular Section 24(b) benefit. Most buyers today do not qualify given the price points of premium Mangaluru projects, but it is worth checking with your CA if you are purchasing a smaller configuration.

What This Means for a Udbhav Chinmaya Buyer

Here is what the tax benefits look like in a single view for a couple buying a 3 BHK at Udbhav Chinmaya on a joint loan under the Old Tax Regime:

That is ₹31.5 Lakhs recovered through tax benefits alone — before accounting for property appreciation, rental income, or the quality-of-life value of living in a premium home at Kadri.

The Bottom Line

The Indian government’s tax framework treats home ownership as a priority — and it shows in the deductions available. But those deductions do not benefit you automatically. They require the right tax regime, the right loan structure, the right co-borrower arrangement, and the right financial year planning.

The smartest Mangaluru buyers in 2026 are not just asking “can I afford this apartment?” They are asking “how much does this apartment actually cost after tax?” That is a very different — and much more encouraging — number.

Disclaimer: This blog is for informational purposes only and does not constitute tax or financial advice. Consult a qualified CA for advice specific to your income, filing status, and tax position.

Starting from ₹1.45 Crore | 3 BHK & 4 BHK | Possession December 2027 RERA No: PRM/KA/RERA/1257/334/PR/311225/008371